A good life guide: Financial Goal Planning & Annual Reflections (with templates)

Chip is a longstanding sponsor of GFY and they’ve kindly sponsored this Good Life guide and some of GFY’s upcoming educational content this January. After many requests for it’s return, they’ve also brought back the free £20 for the GFY community.

Call me a cliché and buy me a ‘live laugh love’ journal but I love a new year planning session. For me, this isn’t about radical transformation or ‘manifestation’ but literally just getting my head straight and setting some direction for the year ahead. It gives me something to aim at and an idea of what I do and don’t want to spend my time worrying about. As a self-employed person, this is vital but if you’re prone to anxiety or worry about money or your direction in work/life, I highly recommend taking an hour or so to think about some of these questions. This guide is geared towards money/work goals but you can use this technique across your personal life too.

Reflections

Take some time to reflect on the last 12 months and answer the following questions. Don’t dwell or beat yourself up about that overpriced holiday or extortionate bus lane fine. Make no value judgements, just pause to reflect.

What was worth the money in the last 12 months?

What was a waste of money in the last 12 months?

What was your greatest financial or career win in the last 12 months?

Are there any habits/lessons you want to take into the next 12 months?

What would you like to do differently or better?

What would you like to leave behind?

Goals

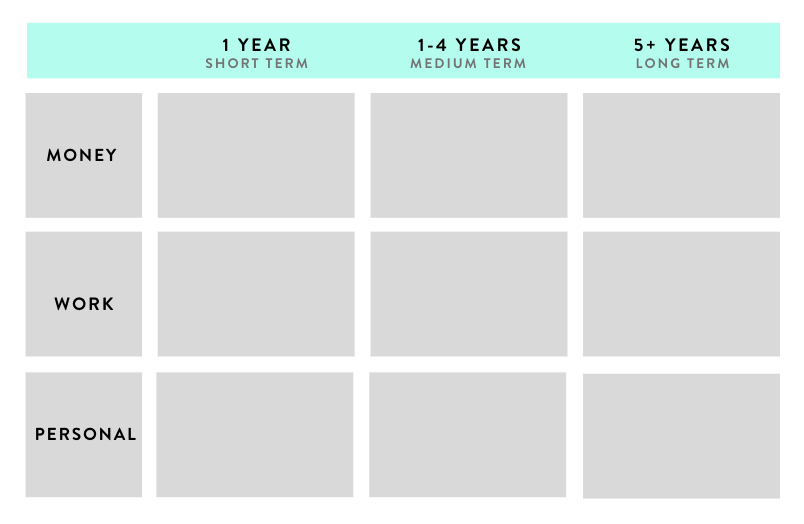

We're now going to look at goal setting. What do you want from your financial, work and personal life? Not just this year, but in the medium and long term too.

How to think about your goals

Ok, so there are two dimensions to your goals:

- Category (e.g. Money, Work or Personal)

- You can personalise this. For example, you may want to expand on ‘personal’ and include things like ‘Relationship’, ‘Friendship’, ‘Health’ and so on. I’ve kept it simple but make it work for you.

- Time (Short, Medium and Long Term)

- In financial terms (when speaking to a financial advisor), 1 year is considered short term and 5 years or more is considered long term enough to consider investing.

You can download this template or draw your own version to include your own categories.

Here are some basic principles to think about when setting your goals.

YOU DO YOU

This is about what you want (not what your family would like, or what you believe other people say is a good idea) Jump off the financial bandwagon and work out what matters to you.

BE SPECIFIC AND REALISTIC

Nail down the details. What does 'going travelling' or ‘financial freedom’ mean financially? 1) What's it going to cost? 2) How long is it going to take to achieve?

PRIORITISE

If you’re struggling to figure out which goals to prioritise, then take a look at this post. Use it to work out your financial priorities. i.e. pay off debt before investing.

REMEMBER INFLATION

Prices rise and the measure of that price rise is called inflation. It’s pretty high right now which is why protecting your cash is so important. If you stash it away in a current account that has an interest rate that is less than inflation, you're technically losing money. You should always keep your emergency fund accessible (which usually means in a very low-interest account) but beyond that, you should look to be smarter with your money.

MAKE IT OFFICIAL

Write down your goals. Start long term and work backwards.

USE TECHNOLOGY

When it comes to sticking to goals, use technology to do the boring or hard stuff. It no longer makes sense or is necessary to try to remember to transfer your savings on payday or to keep track of multiple current accounts for different things. There are a tonne of brilliant solutions out that can do all of this for you. Unless you really love excel (hats off to you), apps really are your friend.

Chip is a brilliant saving app that connects to your bank account, automatically builds your savings and fights to bring you the best rates of interest. Think Payday Put Away, saving rules and goals 👌

They’re also a longstanding sponsor of GFY and have kindly sponsored this Good Life guide and some of GFY’s upcoming educational content this January. Following on from the GFY Christmas Challenge they’re bringing back the £20 gift for the GFY community and have a £20k giveaway you can join.

How to get the £20

✅ You’re a new customer to Chip

✅ Download the Chip app and use code GFY22 (profile > earn and track rewards)

✅ Connect your bank and save at least £1. The offer is available on all Chip plans (including Chip's free plan)

✅ You’ll receive your £20 on the 12/03/22

T&C's and eligibility criteria apply please click here for T&Cs

How to join the giveaway

Click this button to join the 20k giveaway

Here are the best bits of the Chip…

Chip is always fighting to bring you the best rates (right now you can get the UK’s best easy-access rate (0.7%)

🗓 Interest is paid daily!

🧙🏻♀️ Save automagically - Chip’s AI can put money aside for you (the average saver automatically saves around £3,000 a year), so you can build savings by doing nothing.

🤑 There are lots of features to encourage you to save up more without noticing, like their Payday Put Away feature, which automatically puts aside extra money on the day you get paid.

🔐 All money you deposit is eligible for the Financial Services Compensation Scheme (FSCS)

👋 They offer customer support 7 days a week and currently have more than 400,000 customers

✅ You can also withdraw your money anytime.

Join the party 🥳

✅ A monthly 💷 round-up straight to your inbox